Negotiating the sale of an Amazon FBA business is a complex process that requires preparation, clear communication, and a solid understanding of the key steps. Both first-time sellers and buyers often feel apprehensive about this stage, but with the right approach, negotiations can lead to a win-win deal. In this guide, we break down the negotiation process step by step and provide tactical advice to help you navigate each stage with confidence. From the initial non-disclosure agreement (NDA) and Letter of Intent (LOI) to the final purchase agreement and closing, we’ll cover what to expect and how to handle each situation.

Pre-Negotiation Preparation for Sellers

Entering a negotiation well-prepared can significantly improve a seller’s chances of a smooth sale. Before talks even begin, a seller should:

- Organize Financials and Performance Data: Have up-to-date financial statements, sales reports, and key metrics ready to share. Accurate, organized data not only supports your asking price but also builds credibility with buyers.

- Know Your Bottom Line: Determine in advance what your ideal price and terms are, as well as the lowest price or most flexible terms you would accept. Deciding on your goals early (e.g. whether you are willing to accept an earnout or stay involved for a transition period) will guide your negotiation strategy.

- Highlight Value Drivers: Identify the strengths of your FBA business – such as strong branding, diversified product lines, or growth opportunities – and be prepared to emphasize these during negotiations. By thinking like a buyer and highlighting key value drivers, you make your business more attractive and justify your valuation.

- Prepare Answers to Common Questions: Expect buyers to ask about supplier relationships, reasons for selling, operations, and risks. Consider conducting a “mock due diligence” on your own business so you can address concerns openly and confidently.

- Protect Confidential Information: Plan how you will share sensitive information. Use NDAs and only reveal critical details (like proprietary product info or supplier lists) once a buyer is vetted and serious. Sharing information incrementally – in the right amounts at the right time – helps protect your business while still engaging genuine buyers.

Pre-Negotiation Preparation for Buyers

Buyers also need to do their homework before entering negotiations. Key preparation steps for a buyer include:

- Research the Business Thoroughly: Before even contacting the seller, study the business listing, its niche, and market trends. Review any prospectus or financial summary provided, and do not ask questions that have obvious answers in the provided materials. Coming in well-informed shows professionalism and respect for the seller’s time.

- Arrange Proof of Funds: Be ready to demonstrate that you have the financial capability to execute the purchase. Sellers (and platforms like exit.io) may require proof of funds or financing pre-approval before sharing detailed financials. Having this ready signals to the seller that you’re serious.

- Know Your Acquisition Criteria: Clarify what you are looking for in terms of business size, revenue, and growth potential. Also decide on your deal-breakers and priorities (e.g. are you focused on a particular ROI, or strategic fit?). This helps in evaluating the deal objectively during negotiations.

- Plan Your Negotiation Strategy: Outline how you will approach offers and counter-offers. For example, decide ahead if you are willing to pay a higher price for favorable terms (such as seller training or financing) or if you will start with a lower offer and negotiate up. However, avoid coming in with an extreme low-ball offer that could sour the discussion – sellers often reject buyers who only focus on the lowest price.

- Engage Advisors Early (if needed): If you’re a first-time buyer, consider consulting with a mentor or advisor who has done acquisitions. They can help you evaluate the business’s value and craft a sensible offer. Also, identify a good attorney to involve once you reach the LOI or contract stage.

Step 1: Initial Contact and NDA

The negotiation process typically begins when a buyer expresses interest in the business. At this stage, an NDA (Non-Disclosure Agreement) is usually signed before detailed information is exchanged. Signing an NDA protects the seller’s confidential data and gives the buyer access to more in-depth materials. For Sellers: Use the NDA stage to vet the buyer – ensure they are qualified and genuinely interested. You might share a teaser or overview of the business first, then after the NDA, provide more sensitive details like financial statements or the Amazon storefront performance. For Buyers: Honor the NDA and respect confidentiality rules. This is also the time to build rapport with the seller: introduce yourself, perhaps share your background and why you’re interested in their FBA business. First impressions count, and sellers may value a buyer who shows professionalism and appreciation for the business beyond just the dollar signs.

Step 2: Sharing Information and Building Trust

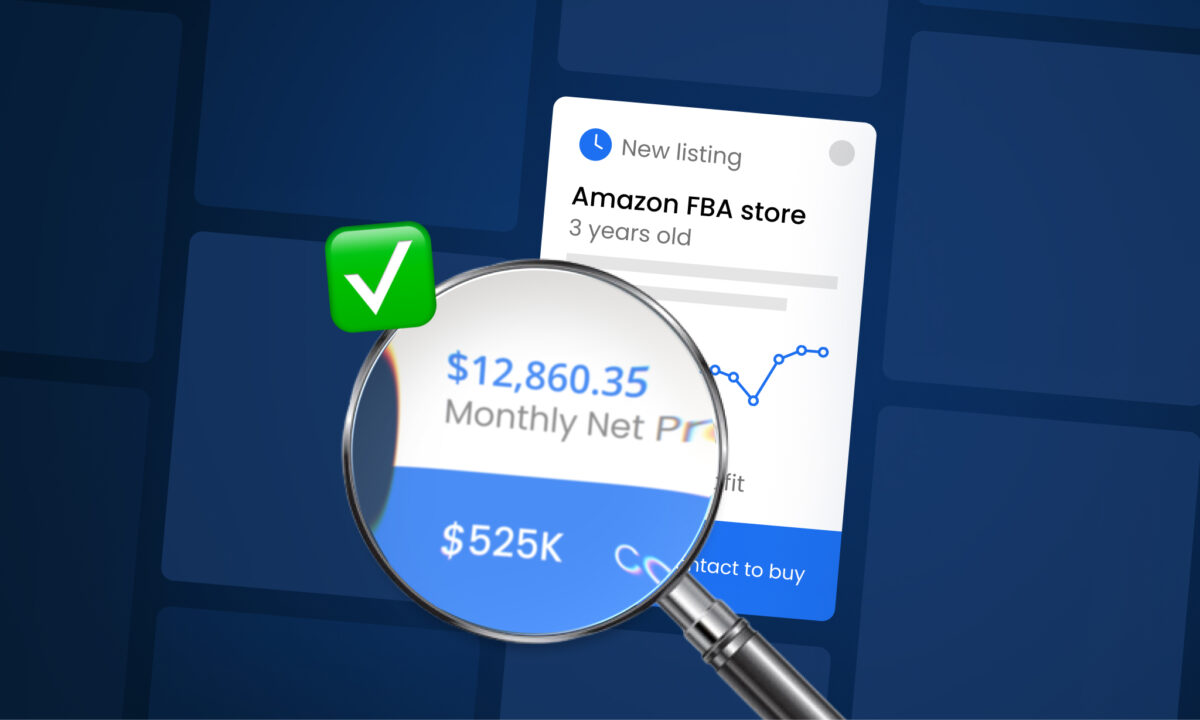

After the NDA is in place, the seller will grant controlled access to important data (for example, detailed financials, product performance reports, or supplier information). On platforms like exit.io, buyers and sellers connect directly through the platform, and sellers can use tools to give read-only access to reports and documents, maintaining control over what is seen and downloaded. At this stage:

- Use Data to Your Advantage: Sellers should be transparent and provide clear, accurate data about the business. Transparency builds trust – when buyers see comprehensive and truthful information, it reassures them and reduces the likelihood of surprises that could derail the deal. Buyers, in turn, should review everything carefully and prepare thoughtful questions.

- Communicate Openly: Both parties should maintain open lines of communication. Buyers, ask questions about anything unclear or any risks you perceive; sellers, answer honestly and promptly. Being forthright about challenges (such as a recent dip in sales or an upcoming inventory expense) can actually build credibility. It shows you’re not hiding anything and are focused on a fair deal.

- Build Personal Rapport: Negotiations aren’t just about numbers. Take time to understand the other side’s motivations. For instance, a seller might be emotionally attached to the brand they built or worried about its legacy. A buyer might be very concerned about how the business will transition to them. A bit of empathy and understanding can go a long way. Remember, negotiation is not a battlefield but a process of discovery for both sides. The more you learn about each other’s goals, the easier it is to find common ground.

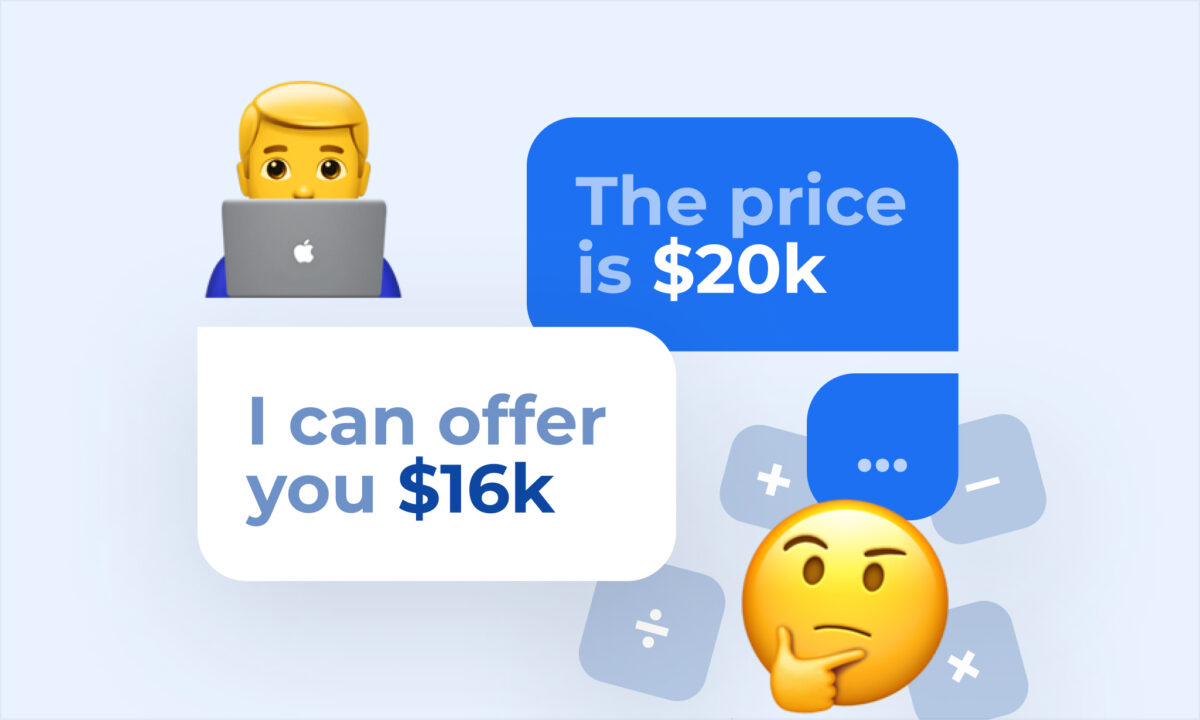

Step 3: Making an Offer and the Letter of Intent (LOI)

Once a buyer has enough information and is interested in moving forward, they will typically make an offer. This often leads to drafting a Letter of Intent (LOI), a document that outlines the key terms of the proposed deal. An LOI usually includes the proposed purchase price, the assets to be included, any anticipated deal structure (e.g. all-cash or with earnouts), a timeline, and usually an exclusivity period during which the seller agrees not to negotiate with others. Importantly, an LOI is generally non-binding – it’s a “preliminary commitment” outlining the broad strokes of the deal before the finer points are resolved. However, even if non-binding, both parties should take the LOI seriously. Only sign an LOI if you are committed to the deal under those terms, barring any major surprises in due diligence.

Tactical Tips for LOI Stage: This is a critical negotiation point:

- Sellers: Don’t hesitate to push back on terms in the LOI that don’t meet your objectives. If the price is lower than you’d like but the buyer is strong, you might counter with a higher price or propose different terms (for example, you accept the price if a larger percentage is paid upfront, or if you keep the inventory separate). Ensure the LOI captures any key points you care about – like your continued involvement post-sale, training period for the buyer, or handling of specific liabilities. Also, be mindful of the exclusivity period; negotiate a reasonable length (e.g. 30-60 days) so that the buyer has enough time for due diligence but you’re not tied up indefinitely.

- Buyers: Make your offer compelling but also leave room for negotiation. Clearly explain the justification for your price and terms (point to the business’s financials, growth, or any risks you’ve factored in). If you offer a lower price than asking, offset it by highlighting the certainty you bring (such as all-cash payment or a quick closing timeline). Avoid any terms that could be seen as overly aggressive or one-sided at this stage – the goal is to get both parties to “yes” on the LOI. Once the LOI is signed, you will have exclusive rights to pursue the deal for the duration of that exclusivity.

Step 4: Due Diligence and Valuation Flexibility

After an LOI is signed, the buyer is given a window (often a few weeks) to conduct due diligence. During due diligence, the buyer scrutinizes the business in depth – reviewing Amazon Seller Central reports, verifying financial statements, checking supplier contracts, inventory, intellectual property, and any other claims made about the business. For sellers, this phase can feel invasive, but it’s crucial to cooperate and provide all information agreed upon. Promptly furnish the documents and data the buyer asks for (as long as they are within the scope of what was agreed). Being transparent now is critical; surprises discovered in due diligence can erode trust or lead to price renegotiation.

Valuation Flexibility: It’s common that due diligence findings may lead to discussions about valuation or deal terms adjustments. Both parties should be a bit flexible here. For example:

- If the business slightly underperforms expectations during due diligence, the buyer might request a price adjustment or an earnout arrangement to cover the gap. Sellers, rather than rejecting this outright, evaluate if the concern is valid and whether structuring part of the price as contingent on future performance is acceptable.

- Conversely, if the business is performing better than expected or the seller can demonstrate additional value (like newly launched profitable products), the seller might justify holding firm on price or even negotiating it upwards.

Remember that both parties want the deal to succeed, and it’s not about “winning” a battle. If each side is willing to compromise and creatively structure the deal, you can often bridge valuation gaps. For instance, you might agree on a middle-ground price but with the seller providing a longer training period, or include an inventory payout separate from the business sale price to satisfy both sides’ financial concerns.

Step 5: Negotiating Deal Structure and the Purchase Agreement

With due diligence nearly completed, the focus turns to finalizing the deal structure and signing the purchase agreement. The deal structure refers to how the sale will be executed:

- Are you doing an asset sale (buying the business’s assets like the Amazon account, inventory, brand, etc.) or a share sale (buying the company entity that owns the business)?

- How will payment be made – all cash at closing, or a mix of upfront payment and deferred payments? Many FBA business sales use a combination of cash and earnout or seller financing; it’s fairly rare in this market for a seller to get 100% cash upfront and walk away completely.

- Will there be an escrow holding period or any hold-back amount to account for things like inventory adjustment or post-sale liabilities?

- What are the responsibilities of the seller after closing (e.g. training the buyer, agreeing to a non-compete period, etc.)?

All these elements are documented in the Asset Purchase Agreement (APA) (or Stock Purchase Agreement, if it’s a share sale). This contract will spell out the final agreed price, payment schedule, assets included, and any representations and warranties by both sides. At this stage, involving a lawyer is crucial. The purchase agreement is a binding legal document that finalizes the terms and conditions of the sale. A lawyer can help ensure the contract protects your interests and that nothing important is missing.

It’s normal for there to be a round of negotiations on the draft purchase agreement. For example, the buyer may request certain warranties about the business’s performance or liabilities, and the seller may negotiate the scope of those promises or the duration of non-compete clauses. Work through these points diligently and try not to let minor issues derail the deal. By this point, both parties have invested significant time – focus on resolving outstanding issues so that both feel comfortable signing.

Step 6: Closing the Deal

Closing is the final step where all the negotiation and preparation pays off. This is when the buyer and seller execute the purchase agreement and the business officially changes hands. Typically, the closing involves:

- Payment Transfer: The buyer transfers the payment as per the agreed terms. Often, a neutral third-party escrow service is used to hold the funds and release them to the seller once all closing conditions are met (this protects both sides).

- Asset Transfer: The seller hands over the assets. For an FBA business, that could include transferring the Amazon Seller Central account (or whatever mechanism is allowed by Amazon to transfer ownership), domain names, customer lists, supplier contacts, inventory (or arrangements for the buyer to take over inventory at Amazon’s warehouses), and any other included assets. Make sure a clear plan is in place for each asset’s transfer.

- Transition and Training: Usually the seller will provide a training period or transition support as outlined in the contract. This might start immediately after closing. Sellers should be prepared to walk the buyer through operations, and buyers should take advantage of this time to learn all the ins and outs of running the FBA business.

- Final Documentation: Both parties should double-check that all required documents are signed and that any platform or legal notifications (for example, informing Amazon of the business ownership change if required) are handled.

Once the deal is closed, congratulations – the negotiation process is complete, and the buyer now owns the business. It’s wise for both parties to maintain a cordial relationship post-sale, at least through the transition period, as questions or minor issues can come up that a friendly dialogue can easily resolve.

Tactical Communication Strategies for Negotiators

Effective communication is the backbone of any successful negotiation. Here are some tactical strategies for both buyers and sellers to ensure the process stays constructive:

- Share Information Strategically: As mentioned, use NDAs and staged information disclosure to protect yourself, but also don’t be so secretive that the other side loses trust. Sellers should be honest about critical facts (financials, challenges) once confidentiality is in place – hiding problems will only hurt you later if uncovered. Buyers should also share relevant information about themselves, such as their business experience or why they are interested in the acquisition, to build credibility.

- Listen and Ask Questions: A good negotiator listens more than they talk. If you’re a buyer, recognize that the business represents more than just numbers to the seller – showing that you appreciate their journey will make them more open to your offer. If you’re a seller, learn what the buyer’s long-term goals are (e.g. a hands-off investment vs. a growth project) – knowing this lets you tailor the deal structure to fit the buyer’s needs.

- Know When to Stand Firm: Identify the non-negotiables in advance – these could be the absolute minimum price you will accept, or a condition like the buyer must take over your office lease. If the other party pushes on a truly critical point, be prepared to assert your position clearly (but respectfully). For buyers, this might mean holding firm on getting certain warranties about the business’s performance; for sellers, it might mean refusing an earnout structure that you find too risky. It’s okay to say “no” to a term that would make you regret the deal.

- Know When to Compromise: Not every point is worth fighting over. Be willing to give ground on lesser issues to gain on more important ones. Both sides should approach negotiation as a collaborative problem-solving exercise rather than a fight. For instance, a buyer might concede on the closing date or a small increase in price if it means the seller will include additional training or assets. A seller might agree to a slightly lower price if the buyer can close quickly or pay mostly in cash. Being rigid on all points can kill a deal, so prioritize your must-haves and be flexible on the rest. The goal is for both parties to feel satisfied with the final outcome.

- Stay Professional and Patient: Emotions can run high in negotiations – especially for sellers who are parting with a business they built, or for buyers investing a large sum. It’s crucial to remain calm, polite, and patient. Avoid aggressive language or ultimatums. If talks stall, sometimes taking a day or two as a “cooling off” period and then revisiting contentious issues with a fresh perspective can help. Keep communication channels open and courteous at all times.

Common Negotiation Pitfalls to Avoid

Negotiating an FBA business sale for the first time is a learning process, and there are common mistakes you should be careful to avoid:

- Going in Unprepared: One major mistake is not knowing what you really want from the sale or purchase. As a seller, if you haven’t thought through your goals (for example, whether you want to stay involved in the business or not, or how you’d feel if the buyer changes the business post-sale), you can end up confused or unhappy with the outcome. As a buyer, not having clear criteria or failing to research the business can lead to overpaying or acquiring a business that isn’t the right fit.

- Letting Price Dominate Everything: Focusing only on the sale price and neglecting other terms is a common pitfall. Negotiation isn’t just about haggling over a number – factors like payment structure, transition support, and contract conditions all contribute to the overall value of the deal. Insisting on a perfect price while ignoring creative deal structures or win-win solutions can backfire. Don’t negotiate in a vacuum; consider the deal as a whole package.

- Poor Information Control: On the sell side, sharing sensitive information with unvetted buyers or too early can backfire. Even with an NDA, if you hand out your supplier list or detailed SKU sales data to anyone who asks, you risk leaks or giving a potential buyer unwarranted leverage. Conversely, buyers who aren’t forthcoming about their ability to close (for example, hiding financing issues) can damage trust. Control the flow of information carefully and vet who you’re dealing with.

- Failure to Involve Advisors at the Right Time: Trying to navigate the entire process alone is risky. For sellers, not having a legal advisor review an LOI or purchase agreement can lead to unfavorable terms or missed liabilities. For buyers, skipping an accountant’s review of financials or not consulting a lawyer on the contract can result in costly surprises. While you don’t need an attorney or CPA in every discussion, bring them in when drafting or reviewing formal documents and definitely before signing anything binding.

- Emotional Decision-Making: Getting too emotionally attached to a position can derail negotiations. Sellers might feel offended by a buyer’s offer and respond harshly, or buyers might get “deal fever” and ignore red flags. It’s important to stay level-headed. Stick to the facts and the business case during discussions. If you feel emotions creeping in, take a step back. Remember, this is a business transaction – professionalism goes a long way in keeping negotiations on track.

Involving Legal and Financial Advisors

Selling or buying an FBA business involves legal and financial complexities, so knowing when to involve professionals is key:

- When to Bring in a Lawyer: For sellers, it’s wise to consult a lawyer once you have a draft Letter of Intent. Even a non-binding LOI can “set a lot of important precedents” for the deal. And certainly, by the time you reach the purchase agreement stage, an experienced attorney should review or help draft it. For buyers, a lawyer can help with structuring the offer in the LOI (to ensure you’re not inadvertently binding yourself to something unintended) and will be essential in reviewing the final contract to make sure your interests are protected.

- Using an Accountant or Financial Advisor: Buyers should consider involving a CPA or financial advisor during due diligence to verify the seller’s financials. They can spot inconsistencies or alert you to any issues in the financial health of the business. Sellers might use a financial advisor early on to help set a realistic valuation and prepare the financial data for presentation.

- Tax and Transition Planning: Both sides may also need advice on tax implications or transition logistics. For instance, how the deal is structured (asset vs. stock sale) can have different tax outcomes – a tax professional can provide guidance here. Also, if the business is sizable, the seller might consult an advisor on how to manage the proceeds post-sale, and the buyer might get advice on post-acquisition financial planning.

- Advisor Involvement During Negotiations: Use advisors as helpers, not as mouthpieces. You ultimately know your goals best. Get expert input to inform your decisions, but avoid sending your lawyer or accountant to negotiate every small detail directly with the other party (unless the deal is large and complex enough to warrant that). Direct buyer-seller communication, backed by professional advice behind the scenes, often keeps the tone more cooperative. Save the heavy involvement of attorneys for drafting and finalizing the legal documents.

How exit.io Supports the Negotiation Phase

If you are using exit.io to buy or sell an Amazon FBA business, the platform is designed to facilitate a safe and direct negotiation process. Buyers and sellers connect directly through exit.io’s system, which fosters clear communication without unnecessary intermediaries. To protect sensitive information, exit.io provides built-in data protection tools:

- Non-Disclosure Agreements: Sellers can require prospective buyers to sign an NDA on the platform before any confidential details are revealed. This ensures that your business data – from product information to financial figures – is legally protected early in the process.

- Controlled Access to Financials: exit.io allows sellers to share financial reports and documents in a controlled way. For example, a seller might upload their profit-and-loss statements or Amazon account screenshots to their listing; interested buyers with an NDA can request access to confidential information, which the seller can approve or deny. This incremental sharing of information (first high-level data, then more detailed data after an offer or LOI) follows best practices to protect the business while still giving buyers what they need to make informed decisions.

- Secure Communication and Escrow Services: The platform offers a secure messaging system for discussing terms and asking questions. Once a deal is agreed upon, exit.io can integrate secure payment or escrow services to ensure that funds and assets change hands safely. This adds an extra layer of trust – buyers know their money is safe until the business is transferred, and sellers know the buyer’s payment is ready.

- Guidance and Resources: exit.io’s marketplace is focused on Amazon businesses, so they provide educational content (like this guide) and support resources to help first-time buyers and sellers. While negotiations are ultimately between the buyer and seller, using a platform experienced in FBA transactions means common hurdles (like Amazon account transfer policies, or setting up escrow) are easier to navigate.

By leveraging these features, exit.io users can negotiate with confidence that their interests are protected and that they’re following a proven process for FBA business sales.

Conclusion: Be Prepared, Be Realistic, and Be Professional

Negotiating an FBA business sale can seem daunting to first-timers, but with thorough preparation and the right mindset, it can be a smooth – even rewarding – process. Remember to prepare diligently, approach discussions with realistic expectations, and maintain professionalism at every step. Both buyer and seller ultimately want a successful transaction: a buyer wants to acquire a thriving business at a fair price, and a seller wants to hand over their enterprise and reap the rewards of their hard work. By focusing on clear communication, mutual respect, and a willingness to compromise, you increase the chances of reaching a deal that satisfies both parties. Keep emotions in check, use data to back up your points, and don’t rush – a well-negotiated deal is far better than a fast but shaky one.

In the end, successful negotiations come down to understanding the other party’s perspective and finding creative solutions to bridge gaps. Whether you’re selling your first Amazon FBA business or buying one, keep the process collaborative. With the guidelines in this article – and with support from platforms like exit.io – you’ll be well equipped to negotiate an FBA business sale confidently and effectively.

Disclaimer: exit.io is a platform that connects buyers and sellers of Amazon businesses. This article is for informational purposes only and does not constitute financial or business advice.